When you’re looking to grow your money safely, a High Yield Savings Account (HYSA) can be your best friend.

Understanding what a High Yield Savings Account is and how it can help you reach your financial goals is crucial. Whether you’re saving for an emergency fund, a dream vacation, or your future, a High Yield Savings Account offers a smart way to make your money work harder for you.

What Is a High Yield Savings Account?

A High Yield Savings Account is a special type of savings account that offers much higher interest rates than traditional savings accounts. Think of it as a regular savings account on steroids – it works the same way (you deposit money and earn interest), but it pays you significantly more for keeping your money there.

Try our High Yield Savings Account Calculator

These accounts are typically offered by online banks, credit unions, or the online divisions of traditional banks. The “high yield” part comes from the fact that they pay interest rates that are often 10 to 12 times higher than what you’d get from a traditional savings account at a brick-and-mortar bank.

How High Yield Savings Accounts Work

High Yield Savings Accounts work on the same basic principle as regular savings accounts: you deposit money, and the bank pays you interest on that money. The key difference is the interest rate (called APY – Annual Percentage Yield) that you earn.

Here’s how it typically works:

- You open an account with a bank or credit union

- You deposit money into the account

- The bank pays you interest on your balance

- You can withdraw money when you need it (with some limits)

- Your interest compounds, meaning you earn interest on your interest

Benefits of a High Yield Savings Account

High Yield Savings Accounts come with several fantastic benefits that make them attractive to savers:

Higher Interest Rates: This is the biggest benefit. While traditional savings accounts might offer 0.39% APY (the national average as of late 2025), High Yield Savings Accounts can offer 3-4.5% APY or even higher. This means your money grows much faster over time.

FDIC Insurance: Just like traditional banks, High Yield Savings Accounts are FDIC insured up to $250,000 per depositor. This means your money is safe even if the bank fails.

Easy Access to Funds: You can typically access your money through online transfers, debit cards, or by linking to your checking account. Many HYSAs also offer ATM cards for easy cash access.

No or Low Fees: Most High Yield Savings Accounts have no monthly maintenance fees and low or no minimum balance requirements, making them accessible to everyone.

Compound Interest: Your interest compounds daily or monthly, which means you earn interest on your interest. This is like a snowball effect that helps your savings grow faster over time.

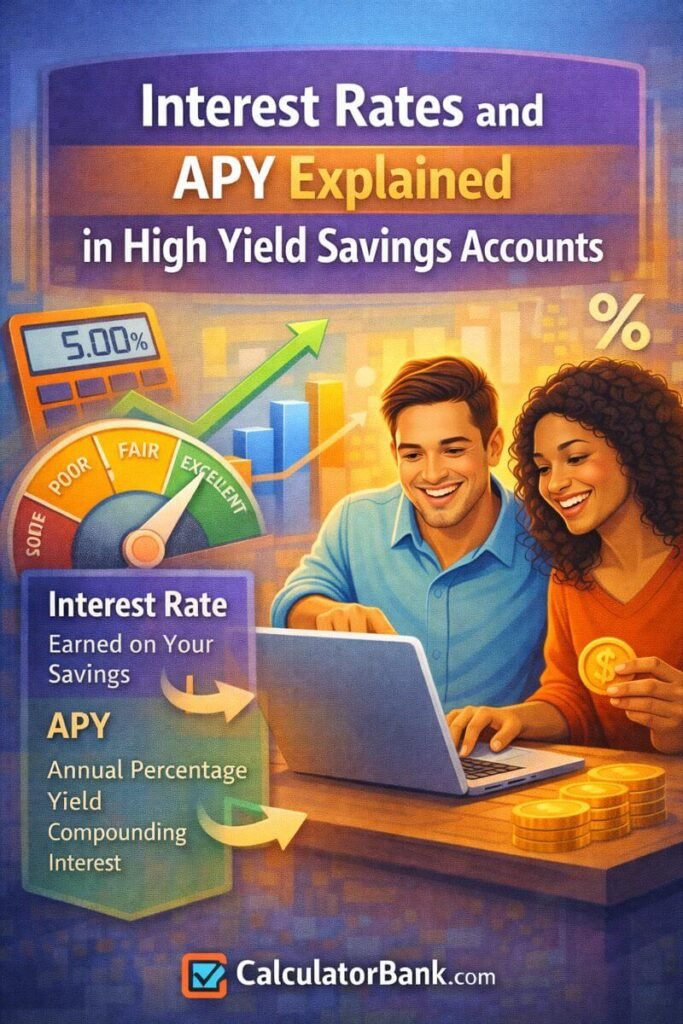

Interest Rates and APY Explained

Understanding interest rates and APY is crucial when it comes to High Yield Savings Accounts. Let me break it down in simple terms:

APY (Annual Percentage Yield): This is the real rate of return you earn on your savings, including the effect of compounding interest. It’s different from a simple interest rate because it accounts for how often interest is added to your account.

For example, if you have $10,000 in a High Yield Savings Account with 4% APY:

- After one year, you’d earn about $400 in interest

- After five years, your $10,000 would grow to about $12,167

- After ten years, it would grow to about $14,802

Compare this to a traditional savings account with 0.39% APY:

- After one year, you’d earn only about $39 in interest

- After five years, your $10,000 would grow to only about $10,198

- After ten years, it would grow to only about $10,401

The difference is huge! That extra interest from a High Yield Savings Account can add up to thousands of dollars over time.

Minimum Balance Requirements

One of the great things about High Yield Savings Accounts is that many of them have very low or no minimum balance requirements. This makes them accessible to people at all income levels.

From my research, here’s what I found about minimum balance requirements:

- Many HYSAs require $0 to open: You can start saving with whatever amount you have

- Some require small minimums: Typically between $5 and $100 to earn the advertised APY

- No monthly fees: Most HYSAs don’t charge monthly maintenance fees, even if your balance drops below a certain level

This is a big advantage over traditional banks, which often require higher minimum balances and charge fees if you don’t maintain them.

Accessibility and Withdrawal Limits

While High Yield Savings Accounts offer great rates, they do have some limitations on how often you can access your money:

Regulation D: Federal law (Regulation D) limits you to six withdrawals or transfers per month from your savings account. This includes:

- Online transfers to your checking account

- Debit card purchases

- Wire transfers

- Checks written from the account

Why this limit exists: Banks use the money in savings accounts to make loans. If too many people withdraw their money at once, it can cause problems for the bank. The six-withdrawal limit helps ensure the bank has enough money to lend.

Ways to access your money:

- Online transfers to your checking account (usually free and fast)

- Debit card (if your HYSA offers one)

- ATM withdrawals (if your HYSA offers an ATM card)

- Wire transfers (may have fees)

High Yield Savings Account vs Traditional Savings Account

Let me show you how High Yield Savings Accounts stack up against traditional savings accounts:

| Feature | High Yield Savings Account | Traditional Savings Account |

|---|---|---|

| Interest Rate (APY) | 3-4.5% (10-12x higher) | 0.39% (national average) |

| Minimum Balance | $0-$100 to open | Often $500-$1,000 |

| Monthly Fees | Usually $0 | Often $5-$15 per month |

| Access | Online, mobile app, sometimes ATM card | Branches, ATMs, online |

| FDIC Insured | Yes, up to $250,000 | Yes, up to $250,000 |

| Compounding | Daily or monthly | Often monthly |

| Best For | Maximizing savings growth | Easy access to branch locations |

High Yield Savings Account vs CDs

While we’re comparing, let’s briefly look at how HYSAs compare to CDs (Certificates of Deposit):

- CDs lock your money for a fixed term (like 6 months, 1 year, or 5 years) and offer a fixed rate

- HYSAs let you access your money (with some limits) and rates can change over time

- CDs typically offer slightly higher rates than HYSAs for the same term

- HYSAs offer more flexibility if you might need to access your money

Considerations Before Opening a High Yield Savings Account

Before you open a High Yield Savings Account, here are some things to think about:

Your Financial Goals: Are you saving for short-term goals (like an emergency fund) or long-term goals? HYSAs are great for both, but you should consider how soon you might need the money.

Bank Reputation: Make sure you choose a reputable bank or credit union. Look for FDIC insurance and good customer reviews.

Fees: Even though most HYSAs have no fees, read the fine print. Some might charge fees for excessive withdrawals or paper statements.

Interest Rate Stability: While HYSAs offer great rates now, remember that rates can change. Online banks may adjust their rates based on what the Federal Reserve does.

Customer Service: Since many HYSAs are online-only, consider how important in-person service is to you. Most offer excellent online and phone support, but it’s different from walking into a branch.

How to Choose the Right High Yield Savings Account

With so many options available, here’s how to choose the best High Yield Savings Account for you:

- Compare Rates: Look for the highest APY you can find

- Check Minimums: Make sure you can meet any minimum balance requirements

- Read Reviews: See what other customers say about the bank’s service

- Consider Features: Do they offer mobile apps, ATM cards, or good online tools?

- Check for Fees: Make sure there are no hidden fees

- Look for Bonuses: Some banks offer sign-up bonuses for new accounts

Tips for Maximizing Your Savings

Here are some practical tips to make the most of your High Yield Savings Account:

Automate Your Savings: Set up automatic transfers from your checking account. Even $50 per week can grow into a substantial amount over time.

Keep an Emergency Fund: Financial experts recommend having 3-6 months of living expenses in an easily accessible account like a HYSA.

Take Advantage of Compounding: The more money you keep in your account, the faster it grows thanks to compound interest.

Shop Around: Rates can change, so it’s worth checking periodically to see if you can get a better rate elsewhere.

Avoid Unnecessary Withdrawals: Try to stay within the six-withdrawal limit to avoid any potential fees.

Common Myths About High Yield Savings Accounts

Let’s clear up some common misconceptions:

Myth: Online banks aren’t safe. Reality: They’re just as safe as traditional banks, thanks to FDIC insurance.

Myth: You can’t access your money easily. Reality: Most HYSAs offer easy online transfers and some offer debit cards.

Myth: You need a lot of money to open one. Reality: Many HYSAs require $0 to open.

Myth: The rates are too good to be true. Reality: Online banks have lower overhead costs, so they can offer better rates.

Conclusion

A High Yield Savings Account is an excellent tool for anyone who wants to grow their money safely and efficiently. With interest rates that are 10-12 times higher than traditional savings accounts, these accounts can help you reach your financial goals faster.

Whether you’re building an emergency fund, saving for a down payment, or just want your money to work harder for you, a High Yield Savings Account is worth considering. The combination of high interest rates, FDIC insurance, and easy access makes them a smart choice for modern savers.

Remember, the key is to start saving early and let compound interest work its magic. Even small amounts can grow into significant sums over time with the power of a High Yield Savings Account.

Take the time to research different options, compare rates, and choose the account that best fits your needs. Your future self will thank you for making your money work harder today!