KEY TAKEAWAY

High-yield savings accounts deliver substantially better returns than conventional savings options, with interest rates ranging from 3% to 4.5% compared to the 0.39% national average.

INTRODUCTION

When searching for ways to grow your savings, a high-yield savings account can be a smart choice—but understanding both advantages and disadvantages is essential before committing. These accounts have surged in popularity recently, delivering substantially better returns than conventional savings options while maintaining security and accessibility.

Today, we break down the pros and cons of a high-yield savings account, helping you make informed decisions about whether this account type aligns with your financial objectives. We’ll examine current rates, features, and constraints to determine if a high-yield account suits your needs.

WHAT IS A HIGH-YIELD SAVINGS ACCOUNT?

A high-yield savings account is a specialized deposit account that delivers substantially better interest earnings than traditional savings products.

These accounts are predominantly offered by online banks and credit unions, which operate with reduced overhead expenses by eliminating physical branch networks. This operational efficiency enables them to share cost savings with customers through enhanced interest rates.

Current Rates: As of 2026, top-performing high-yield savings accounts deliver APYs (Annual Percentage Yields) ranging from 3% to 4.5%, compared to the national average of 0.39% for conventional savings accounts. This translates to earning 8-12 times more interest with a high-yield account!

Try using High Yield Savings Account Calculator

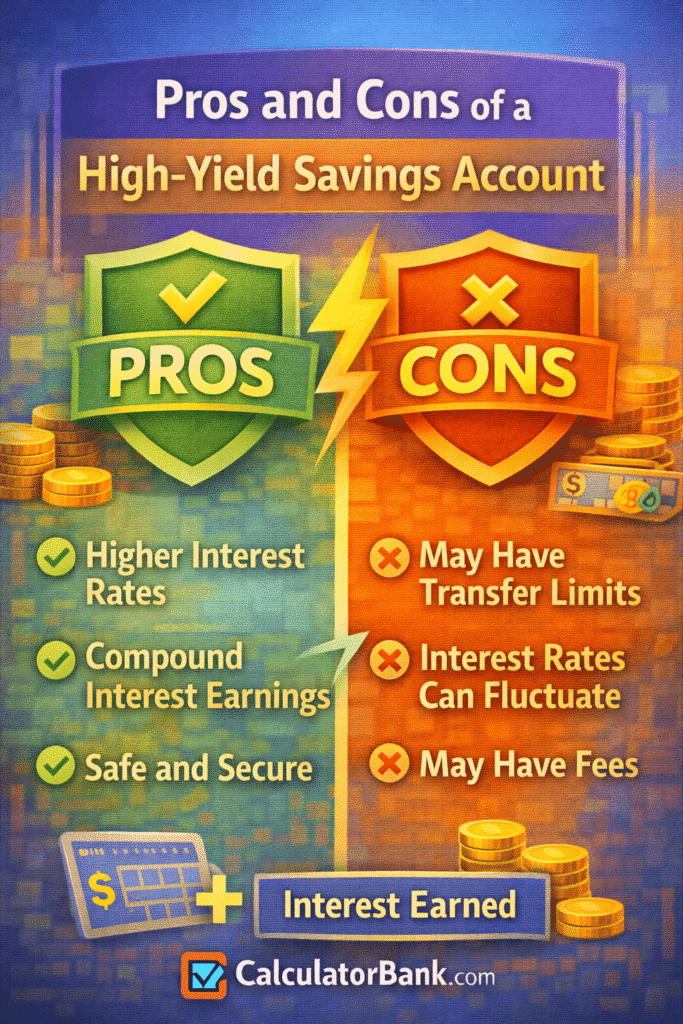

THE PROS OF HIGH-YIELD SAVINGS ACCOUNTS

Higher Interest Rates

The most compelling benefit of high-yield savings accounts is the substantially elevated interest rates they provide. While conventional savings accounts pay around 0.39% APY, high-yield accounts currently deliver 3-4.5% APY or higher.

Related Post: How Interest Is Calculated on High-Yield Savings Accounts

Why this matters: Consider having $10,000 in savings. A traditional account earning 0.39% APY would generate roughly $39 in annual interest. That same deposit in a high-yield account earning 4% APY would produce $400—more than 10 times greater!

Low or No Fees

The majority of high-yield savings accounts eliminate monthly maintenance charges and require minimal or no minimum balance. This accessibility benefits savers across all income levels, unlike many traditional banks imposing monthly fees and demanding higher minimum balances.

FDIC or NCUA Insurance

Similar to traditional banks, high-yield savings accounts carry federal insurance protection. With FDIC insurance (for banks) or NCUA insurance (for credit unions), deposits are protected up to $250,000 per depositor. Your money remains secure even if the institution fails.

Daily Compounding

Most high-yield savings accounts utilize daily compounding, meaning interest is calculated and added to your balance every day. This creates faster growth compared to accounts compounding interest less frequently.

Easy Online Access

High-yield savings accounts are built for online banking, providing 24/7 account access through websites or mobile apps. Many also include features like:

- Online transfers to checking accounts

- Mobile check deposit

- Bill pay services

- Budgeting tools

No Impact on Your Credit Score

Opening a high-yield savings account won’t affect your credit score, unlike certain other financial products. This makes them ideal for building savings without credit-related concerns.

Better Than Inflation

With inflation currently around 3-4%, a high-yield savings account earning 4% APY helps your money keep pace with or even outpace inflation, preserving your purchasing power over time.

THE CONS OF HIGH-YIELD SAVINGS ACCOUNTS

Online-Only Access

Most high-yield savings accounts are offered by online-only banks, which means:

- No physical branch locations for in-person service

- Limited or no ATM access (though some provide debit cards)

- Customer service primarily through phone, chat, or email

This can create inconvenience if you prefer face-to-face banking or need immediate assistance.

Withdrawal Limits

High-yield savings accounts are governed by Regulation D, limiting you to six withdrawals or transfers monthly. While this restriction rarely impacts most savers, it can become problematic if you need frequent account access.

Rate Variability

Unlike certificates of deposit with fixed rates, high-yield savings account rates fluctuate over time. When the Federal Reserve adjusts interest rates, banks often modify their account rates accordingly.

Potential for Lower Rates

While current rates appear attractive, they may decline in the future. If you open an account today with 4% APY, that rate could drop next year depending on economic conditions.

Slower Transfers

Transfers between your high-yield savings account and checking account may require 2-3 business days to complete, unlike instant transfers within the same banking institution.

Less Integrated Services

Many high-yield savings accounts don’t provide the comprehensive service suite offered by traditional banks, such as:

- Credit cards

- Mortgage loans

- Investment services

- Business banking

Minimum Opening Deposits

While many accounts have low minimums, some require initial deposits to open the account, typically ranging from $100 to $500.

WHO BENEFITS MOST FROM HIGH-YIELD SAVINGS ACCOUNTS?

Ideal Candidates

High-yield savings accounts are particularly beneficial for:

- Emergency fund builders: Higher interest accelerates emergency savings growth

- Short-term savers: Those saving for goals within 1-3 years (vacations, down payments, etc.)

- Online banking users: People comfortable with digital banking

- Inflation-conscious savers: Those wanting to preserve purchasing power

- Rate shoppers: People who compare and switch accounts for better rates

Try using the Emergency Fund Calculator

Who Might Want to Look Elsewhere

You might prefer a traditional savings account if you:

- Need frequent branch access

- Make more than six withdrawals monthly

- Prefer consolidating all accounts at one bank

- Want guaranteed long-term rates

- Need immediate access to funds

How To Maximize The Benefits Of High-Yield Savings Accounts

Shop Around for Rates

Interest rates on high-yield savings accounts vary significantly between institutions. Take time comparing rates and features before selecting an account.

Consider Your Goals

Match the account to your specific savings objectives. High-yield accounts excel for emergency funds and short-term goals, but other accounts might better serve long-term savings.

Automate Your Savings

Establish automatic transfers to your high-yield savings account. Even small, regular deposits can grow substantially over time through compound interest.

Monitor Rate Changes

Keep track of your account’s APY. If rates decline significantly, you may want to consider switching to a different account with better returns.

Understand the Rules

Familiarize yourself with withdrawal limits and other account restrictions to avoid unexpected fees or complications.

CURRENT HIGH-YIELD SAVINGS ACCOUNT EXAMPLES

Here are some examples of top high-yield savings accounts as of 2026:

- Newtek Bank: 4.35% APY, no minimum to open, no monthly fee

- Openbank: 4.20% APY, $500 minimum deposit, no monthly fee

- Vio Bank: 4.02% APY, $100 minimum deposit

- Bread Savings: 4.00% APY, $100 minimum deposit

- Capital One Performance 360: 3.30% APY, no minimum balance

FINAL CONSIDERATIONS

When deciding whether a high-yield savings account is right for you, weigh the pros and cons based on your individual needs and preferences. For most savers, the higher interest rates and low fees make high-yield accounts an excellent choice for growing savings safely.

Remember that the best account for you depends on your specific financial situation, goals, and banking preferences. Take time researching different options and choose an account that aligns with your needs.

SUMMARY

Pros: Higher interest rates, low fees, FDIC insurance, daily compounding, online access

Cons: Online-only access, withdrawal limits, rate variability, slower transfers

Best for: Emergency funds, short-term savings, online banking users

Current rates: 3-4.5% APY vs. 0.39% average for traditional accounts

FDIC protection: Up to $250,000 per depositor

A high-yield savings account can be a powerful tool for growing your savings, but it’s important to understand both the benefits and limitations before opening one.